About the CoMSES Model Library more info

Our mission is to help computational modelers at all levels engage in the establishment and adoption of community standards and good practices for developing and sharing computational models. Model authors can freely publish their model source code in the Computational Model Library alongside narrative documentation, open science metadata, and other emerging open science norms that facilitate software citation, reproducibility, interoperability, and reuse. Model authors can also request peer review of their computational models to receive a DOI.

All users of models published in the library must cite model authors when they use and benefit from their code.

Please check out our model publishing tutorial and contact us if you have any questions or concerns about publishing your model(s) in the Computational Model Library.

We also maintain a curated database of over 7500 publications of agent-based and individual based models with additional detailed metadata on availability of code and bibliometric information on the landscape of ABM/IBM publications that we welcome you to explore.

Displaying 10 of 67 results Households clear search

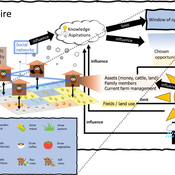

3spire: an agent-based model for exploring aspiration adaptation theory and its implications on smallholder farmers in Ethiopia

ateeuw Yue Dou Markus A Meyer Andrew Nelson | Published Sunday, February 16, 20253spire is an ABM where farming households make management decisions aimed at satisficing along the aspirational dimensions: food self-sufficiency, income, and leisure. Households decision outcomes depend on their social networks, knowledge, assets, household needs, past management, and climate/market trends

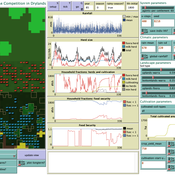

Peer reviewed LUCID: Land Use Competition In Drylands

Gunnar Dressler Birgit Müller Lance Robinson | Published Wednesday, April 12, 2023The Land Use Competition in Drylands (LUCID) model is a stylized agent-based model of a smallholder farming system. Its main purpose is to illustrate how competition between pastoralism and crop cultivation can affect livelihoods of households, specifically their food security. In particular, the model analyzes whether the expansion of crop cultivation may contribute to a vicious circle where an increase in cultivated area leads to higher grazing pressure on the remaining pastureland, which in turn may cause forage shortages and livestock loss for households which are then forced to further expand their cultivated area in order to increase their food security. The model does not attempt to replicate a particular case study but to generate a general understanding of mechanisms and drivers of such vicious circles and to identify possible scenarios under which such circles may be prevented.

The model is inspired by observations of the Borana land use system in Southern Ethiopia. The climatic and ecological conditions of the Borana zone favor pastoralism, and traditionally livelihoods have been based mainly on livestock keeping. Recent years, however, have seen an advancement of crop cultivation as a coping strategy, e.g., to compensate the loss of livestock, even though crop yields are low on average and successful harvests are infrequent.

In the model, it is possible to evaluate patterns of individual (single household) as well as overall (across all households) consumption and food security, depending on a range of ecological, climatic and management parameters.

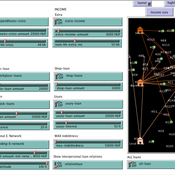

Peer reviewed Credit and debt market of low-income families

Márton Gosztonyi | Published Tuesday, December 12, 2023 | Last modified Friday, January 19, 2024The purpose of the Credit and debt market of low-income families model is to help the user examine how the financial market of low-income families works.

The model is calibrated based on real-time data which was collected in a small disadvantaged village in Hungary it contains 159 households’ social network and attributes data.

The simulation models the households’ money liquidity, expenses and revenue structures as well as the formal and informal loan institutions based on their network connections. The model forms an intertwined system integrated in the families’ local socioeconomic context through which families handle financial crises and overcome their livelihood challenges from one month to another.

The simulation-based on the abstract model of low-income families’ financial survival system at the bottom of the pyramid, which was described in following the papers:

…

Peer reviewed Coupled demographic dynamics of herd and household in pastoral systems

Chelsea E Hunter Daniel C Peart Abigail Buffington Andrew Yoak Ian M Hamilton Mark Moritz | Published Saturday, April 08, 2023This purpose of this model is to understand how the coupled demographic dynamics of herds and households constrain the growth of livestock populations in pastoral systems.

Peer reviewed Labor and environment in global value chains: An evolutionary policy study with a three-sector and two-region agent-based macroeconomic model

Lena Gerdes Bernhard Rengs Manuel Scholz-Wäckerle | Published Wednesday, December 22, 2021With this model, we investigate resource extraction and labor conditions in the Global South as well as implications for climate change originating from industry emissions in the North. The model serves as a testbed for simulation experiments with evolutionary political economic policies addressing these issues. In the model, heterogeneous agents interact in a self-organizing and endogenously developing economy. The economy contains two distinct regions – an abstract Global South and Global North. There are three interlinked sectors, the consumption good–, capital good–, and resource production sector. Each region contains an independent consumption good sector, with domestic demand for final goods. They produce a fictitious consumption good basket, and sell it to the households in the respective region. The other sectors are only present in one region. The capital good sector is only found in the Global North, meaning capital goods (i.e. machines) are exclusively produced there, but are traded to the foreign as well as the domestic market as an intermediary. For the production of machines, the capital good firms need labor, machines themselves and resources. The resource production sector, on the other hand, is only located in the Global South. Mines extract resources and export them to the capital firms in the North. For the extraction of resources, the mines need labor and machines. In all three sectors, prices, wages, number of workers and physical capital of the firms develop independently throughout the simulation. To test policies, an international institution is introduced sanctioning the polluting extractivist sector in the Global South as well as the emitting industrial capital good producers in the North with the aim of subsidizing innovation reducing environmental and social impacts.

Peer reviewed Co-adoption of low-carbon household energy technologies

Mart van der Kam Maria Lagomarsino Elie Azar Ulf Hahnel David Parra | Published Tuesday, August 29, 2023 | Last modified Friday, February 23, 2024The model simulates the diffusion of four low-carbon energy technologies among households: photovoltaic (PV) solar panels, electric vehicles (EVs), heat pumps, and home batteries. We model household decision making as the decision marking of one person, the agent. The agent decides whether to adopt these technologies. Hereby, the model can be used to study co-adoption behaviour, thereby going beyond traditional diffusion models that focus on the adop-tion of single technologies. The combination of these technologies is of particular interest be-cause (1) using the energy generated by PV solar panels for EVs and heat pumps can reduce emissions associated with transport and heating, respectively, and (2) EVs, heat pumps, and home batteries can help to integrate PV solar panels in local electricity grids by offering flexible demand (EVs and heat pumps) and energy storage (home batteries and EVs), thereby reducing grid impacts and associated upgrading costs.

The purpose of the model is to represent realistic adoption and co-adoption behaviour. This is achieved by grounding the decision model on the risks-as-feelings model (Loewenstein et al., 2001), theory from environmental and social psychology, and empirically informing agent be-haviour by survey-data among 1469 people in the Swiss region Romandie.

The model can be used to construct scenarios for the diffusion of the four low-carbon energy technologies depending on different contexts, and as a virtual experimentation environment for ex ante evaluation of policy interventions to stimulate adoption and co-adoption.

Peer reviewed Modern Wage Dynamics

J M Applegate | Published Sunday, June 05, 2022The Modern Wage Dynamics Model is a generative model of coupled economic production and allocation systems. Each simulation describes a series of interactions between a single aggregate firm and a set of households through both labour and goods markets. The firm produces a representative consumption good using labour provided by the households, who in turn purchase these goods as desired using wages earned, thus the coupling.

Each model iteration the firm decides wage, price and labour hours requested. Given price and wage, households decide hours worked based on their utility function for leisure and consumption. A labour market construct chooses the minimum of hours required and aggregate hours supplied. The firm then uses these inputs to produce goods. Given the hours actually worked, the households decide actual consumption and a market chooses the minimum of goods supplied and aggregate demand. The firm uses information gained through observing market transactions about consumption demand to refine their conceptions of the population’s demand.

The purpose of this model is to explore the general behaviour of an economy with coupled production and allocation systems, as well as to explore the effects of various policies on wage and production, such as minimum wage, tax credits, unemployment benefits, and universal income.

…

Peer reviewed PolicySpace2: modeling markets and endogenous public policies

Bernardo Furtado | Published Thursday, February 25, 2021 | Last modified Friday, January 14, 2022Policymakers decide on alternative policies facing restricted budgets and uncertain future. Designing public policies is further difficult due to the need to decide on priorities and handle effects across policies. Housing policies, specifically, involve heterogeneous characteristics of properties themselves and the intricacy of housing markets and the spatial context of cities. We propose PolicySpace2 (PS2) as an adapted and extended version of the open source PolicySpace agent-based model. PS2 is a computer simulation that relies on empirically detailed spatial data to model real estate, along with labor, credit, and goods and services markets. Interaction among workers, firms, a bank, households and municipalities follow the literature benchmarks to integrate economic, spatial and transport scholarship. PS2 is applied to a comparison among three competing public policies aimed at reducing inequality and alleviating poverty: (a) house acquisition by the government and distribution to lower income households, (b) rental vouchers, and (c) monetary aid. Within the model context, the monetary aid, that is, smaller amounts of help for a larger number of households, makes the economy perform better in terms of production, consumption, reduction of inequality, and maintenance of financial duties. PS2 as such is also a framework that may be further adapted to a number of related research questions.

Peer reviewed Swidden Farming Version 2.0

C Michael Barton | Published Wednesday, June 12, 2013 | Last modified Wednesday, September 03, 2014Model of shifting cultivation. All parameters can be controlled by the user or the model can be run in adaptive mode, in which agents innovate and select parameters.

Peer reviewed BAM: The Bottom-up Adaptive Macroeconomics Model

Alejandro Guerra-Hernández Alejandro Platas López | Published Tuesday, January 14, 2020 | Last modified Sunday, July 26, 2020Overview

Purpose

Modeling an economy with stable macro signals, that works as a benchmark for studying the effects of the agent activities, e.g. extortion, at the service of the elaboration of public policies..

…

Displaying 10 of 67 results Households clear search