A financial market with zero intelligence agents (1.0.0)

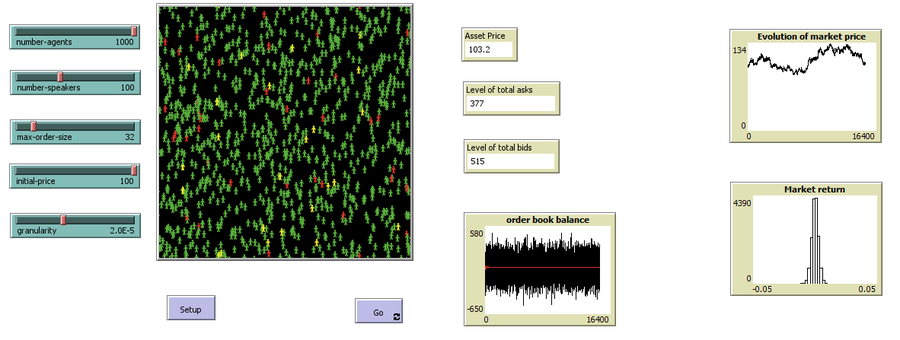

The model’s aim is to represent the price dynamics under very simple market conditions, given the values adopted by the user for the model parameters. We suppose the market of a financial asset contains agents on the hypothesis they have zero-intelligence. In each period, a certain amount of agents are randomly selected to participate to the market. Each of these agents decides, in a equiprobable way, between proposing to make a transaction (talk = 1) or not (talk = 0). Again in an equiprobable way, each participating agent decides to speak on the supply (ask) or the demand side (bid) of the market, and proposes a volume of assets, where this number is drawn randomly from a uniform distribution. The granularity depends on various factors, including market conventions, the type of assets or goods being traded, and regulatory requirements. In some markets, high granularity is essential to capture small price movements accurately, while in others, coarser granularity is sufficient due to the nature of the assets or goods being traded

Release Notes

It is a first release of the project

Associated Publications

A financial market with zero intelligence agents 1.0.0

Submitted byedgarkpPublished Mar 27, 2024

Last modified Dec 05, 2024

The model’s aim is to represent the price dynamics under very simple market conditions, given the values adopted by the user for the model parameters. We suppose the market of a financial asset contains agents on the hypothesis they have zero-intelligence. In each period, a certain amount of agents are randomly selected to participate to the market. Each of these agents decides, in a equiprobable way, between proposing to make a transaction (talk = 1) or not (talk = 0). Again in an equiprobable way, each participating agent decides to speak on the supply (ask) or the demand side (bid) of the market, and proposes a volume of assets, where this number is drawn randomly from a uniform distribution. The granularity depends on various factors, including market conventions, the type of assets or goods being traded, and regulatory requirements. In some markets, high granularity is essential to capture small price movements accurately, while in others, coarser granularity is sufficient due to the nature of the assets or goods being traded

Release Notes

It is a first release of the project

Cite this Model

edgarkp (2024, March 27). “A financial market with zero intelligence agents” (Version 1.0.0). CoMSES Computational Model Library. Retrieved from: https://doi.org/10.25937/8wym-em13

References

Economy as a complex adaptive system (CAS), Murat Yıldızoglu, Pre-conference workshop on Agent-based Models in Economics and Finance, CEF 2015 Conference, Taipei

Create an Open Code Badge that links to this model more info

This website uses cookies and Google Analytics to help us track user engagement and improve our site. If

you'd like to know more information about what data we collect and why, please see

our data privacy policy. If you continue to use this site, you consent to

our use of cookies.